Activity Ratios, Efficiency Ratios (Показатели оборачиваемости, коэффициенты деловой активности)

Activity Ratios (Efficiency Ratios) (Коэффициенты деловой активности) позволяют проанализировать, насколько эффективно компания использует собственные средства.

Receivable Turnover (Оборачиваемость дебиторской задолженности)

Accounts Payable Turnover (Оборачиваемость кредиторской задолженности)

Payables Conversion Period (Период погашения кредиторской задолженности)

Working Capital Turnover (Оборачиваемость собственного оборотного капитала)

Показатели особенно важно сравнивать со средне отраслевыми значениями, так как их величина может существенно колебаться в зависимости от отрасли.

Inventory Turnover

Inventory turnover (Оборачиваемость запасов) показывает, сколько раз за анализируемый период компания использовала средний имеющийся остаток запасов.

Inventory turnover = Sales / Inventory

Inventory turnover = Cost of goods sold / Average inventory

Inventory turnover = Себестоимость продаж / Среднегодовой остаток запасов

Чем выше оборачиваемость запасов компании, тем более эффективным является производство и тем меньше потребность в оборотном капитале для его организации. Особенно актуально повышение оборачиваемости и снижение запасов при наличии значительной задолженности в пассивах компании.

Для расчета показателя оборачиваемости запасов в днях необходимо 365 дней разделить на значение коэффициента:

Days’ sales in Inventory (Период оборота запасов) = 365 / Inventory turnover

Days inventory outstanding = (Inventory / Cost of sales) * 365

Receivable Turnover

Receivable turnover ratio (Оборачиваемость дебиторской задолженности) характеризует скорость оплаты дебиторской задолженности компании, то есть насколько быстро компания получает оплату за проданные товары (работы, услуги) от своих покупателей.

Receivables turnover = Net credit sales / average net receivables

Accounts receivable turnover ratio = Net annual credit sales / (Beginning accounts receivable + ending accounts receivable) / 2

Receivables turnover = Выручка / Средний остаток дебиторской задолженности

Коэффициент определяет эффективность работы компании с покупателями и заказчиками в части взыскания дебиторской задолженности, а также отражает политику в отношении продаж в кредит.

Receivables Conversion Period

Receivables conversion period, Average collection period (Период погашения дебиторской задолженности). Показывает среднее число дней, требуемое для взыскания задолженности. Чем меньше это число, тем быстрее дебиторская задолженность обращается в денежные средства, а следовательно, повышается ликвидность оборотных средств предприятия.

Receivables conversion period = Account receivables / (Annual credit sales / 365)

Average collection period = (365 * Average amount of accounts receivables) / Total amount of net credit sales during period

Average collection period = 365 / Receivables turnover

Чем меньше это число, тем быстрее дебиторская задолженность обращается в денежные средства, а, следовательно, повышается ликвидность оборотных средств компании. Высокое значение показателя может свидетельствовать о трудностях с взысканием средств по счетам дебиторов.

Accounts Payable Turnover

Accounts payable turnover (Оборачиваемость кредиторской задолженности), характеризует скорость погашения кредиторской задолженности перед поставщиками и подрядчиками.

Коэффициент применяется для количественной оценки скорости, с которой компания оплачивает собственную задолженность.

Accounts payable turnover = Total supplier purchases / Average accounts payable

Accounts payable turnover = Сумма счетов предъявленных поставщиками за период / Средняя сумма кредиторской задолженности

Как и оборачиваемость дебиторской задолженности, показатель служит для оценки денежных потоков компании, эффективности ее расчетов.

Поскольку показатель Total supplier purchases не раскрывается в бухгалтерской отчетности, то можно воспользоваться упрощенным вариантом расчета:

Payables Conversion Period

Для определения показателя Payables conversion period (Период погашения кредиторской задолженности) в днях применяется формула, имеющая вид:

Payables conversion period = 365 / Accounts payable turnover

Payables conversion period = (Accounts payables / purchases) * 365

Показатель позволяет определить, насколько быстро компания оплачивает счета поставщиков. Резкое повышение показателя может указывать на проблемы с притоком денежной наличности, а снижение – на досрочную оплату счетов с целью получения скидки

Cash Conversion Cycle

Cash conversion cycle, Operating cycle (Денежный цикл, или цикл оборотного капитала) – это период обращения денежных средств компании с момента приобретения за них ресурсов (сырья, материалов или рабочей силы) и до момента продажи готовой продукции и получения за товар денег.

Cash conversion cycle = Оборачиваемость запасов в днях + Оборачиваемость дебиторской задолженности в днях – Оборачиваемость кредиторской задолженности в днях

Данный показатель выражается в днях и отражает эффективность управления оборотным капиталом компании. Чем короче денежный цикл, тем выше ликвидность компании.

Asset Turnover

Asset turnover (Оборачиваемость активов) – показатель интенсивности использования компанией всех имеющихся активов.

Asset turnover = Net sales or Revenues / Total assets

Asset turnover = Выручка / Среднегодовая стоимость активов

Если необходимо определить оборачиваемость в днях, то формула показателя примет вид:

Asset turnover in days = 365 / Asset turnover

Характеризует эффективность использования ресурсов, привлеченных для организации производства. Является показателем, косвенно отражающим потенциальную рентабельность работы компании. Данный коэффициент показывает сколько раз за год совершается полный цикл производства и обращения, приносящий соответствующий эффект в виде прибыли. Этот коэффициент также сильно варьируется в зависимости от отрасли.

Working Capital Turnover

Working capital turnover (Оборачиваемость собственного оборотного капитала). Показывает, насколько эффективно компания использует инвестиции в рабочий капитал и как это влияет на рост объемов продаж. Чем выше значение этого показателя, тем более эффективно используется компанией рабочий капитал.

Working capital turnover = Sales or Revenue / (Opening working capital + closing working capital)/2

Working capital turnover = Объем продаж / Средняя величина собственных оборотных средств

В российской практике показатель Working capital известен под названием «Собственные оборотные средства».

Fixed Assets Turnover

Fixed assets turnover (Фондоотдача) это показатель применяемый для характеристики динамики эффективности использования основных средств компании, а также для сравнительной оценки эффективности использования основных фондов на предприятиях одной отрасли.

Fixed assets turnover = Net sales / Net property, plan, equipment

Fixed assets turnover = Выручка / Среднегодовая стоимость основных производственных фондов

Этот коэффициент характеризует эффективность использования предприятием имеющихся в его распоряжении основных средств. Чем выше значение коэффициента, тем более эффективно предприятие использует основные средства. Низкий уровень фондоотдачи свидетельствует о недостаточном объеме продаж или о слишком высоком уровне капитальных вложений.

Однако значения данного коэффициента сильно отличаются друг от друга в различных отраслях. Также значение данного коэффициента сильно зависит от способов начисления амортизации и практики оценки стоимости активов.

Days Sales of Inventory – DSI

:max_bytes(150000):strip_icc()/adam_hayes-5bfc262a46e0fb005118b414.jpg)

:max_bytes(150000):strip_icc()/PortraitHeadshot-DavidKindness-DavidKindness-2318e84654364a0584b715e44c99f13a.jpg)

What Is Days Sales Of Inventory – DSI?

The days sales of inventory (DSI) is a financial ratio that indicates the average time in days that a company takes to turn its inventory, including goods that are a work in progress, into sales.

DSI is also known as the average age of inventory, days inventory outstanding (DIO), days in inventory (DII), days sales in inventory or days inventory and is interpreted in multiple ways. Indicating the liquidity of the inventory, the figure represents how many days a company’s current stock of inventory will last. Generally, a lower DSI is preferred as it indicates a shorter duration to clear off the inventory, though the average DSI varies from one industry to another.

Days Sales of Inventory

Formula and Calculating DSI

To manufacture a salable product, a company needs raw material and other resources which form the inventory and come at a cost. Additionally, there is a cost linked to the manufacturing of the salable product using the inventory. Such costs include labor costs and payments towards utilities like electricity, which is represented by the cost of goods sold (COGS) and is defined as the cost of acquiring or manufacturing the products that a company sells during a period. DSI is calculated based on the average value of the inventory and cost of goods sold during a given period or as of a particular date. Mathematically, the number of days in the corresponding period is calculated using 365 for a year and 90 for a quarter. In some cases, 360 days is used instead.

The numerator figure represents the valuation of the inventory. The denominator (Cost of Sales / Number of Days) represents the average per day cost being spent by the company for manufacturing a salable product. The net factor gives the average number of days taken by the company to clear the inventory it possesses.

Two different versions of the DSI formula can be used depending upon the accounting practices. In the first version, the average inventory amount is taken as the figure reported at the end of the accounting period, such as at the end of the fiscal year ending June 30. This version represents DSI value “as of” the mentioned date. In another version, the average value of Start Date Inventory and End Date Inventory is taken, and the resulting figure represents DSI value “during” that particular period. Therefore,

COGS value remains the same in both the versions.

Key Takeaways

What DSI Tells You

Since DSI indicates the duration of time a company’s cash is tied up in its inventory, a smaller value of DSI is preferred. A smaller number indicates that a company is more efficiently and frequently selling off its inventory, which means rapid turnover leading to the potential for higher profits (assuming that sales are being made in profit). On the other hand, a large DSI value indicates that the company may be struggling with obsolete, high-volume inventory and may have invested too much into the same. It is also possible that the company may be retaining high inventory levels in order to achieve high order fulfillment rates, such as in anticipation of bumper sales during an upcoming holiday season.

DSI is a measure of the effectiveness of inventory management by a company. Inventory forms a significant chunk of the operational capital requirements for a business. By calculating the number of days that a company holds onto the inventory before it is able to sell it, this efficiency ratio measures the average length of time that a company’s cash is locked up in the inventory.

However, this number should be looked upon cautiously as it often lacks context. DSI tends to vary greatly among industries depending on various factors like product type and business model. Therefore, it is important to compare the value among the same sector peer companies. Companies in the technology, automobile, and furniture sectors can afford to hold on to their inventories for long, but those in the business of perishable or fast moving consumer goods (FMCG) cannot. Therefore, sector-specific comparisons should be made for DSI values.

One must also note that a high DSI value may be preferred at times depending on the market dynamics. If a short supply is expected for a particular product in the next quarter, a business may be better off holding on to its inventory and then selling it later for a much higher price, thus leading to improved profits in the long run.

For example, a drought situation in a particular soft water region may mean that authorities will be forced to supply water from another area where water quality is hard. It may lead to a surge in demand for water purifiers after a certain period, which may benefit the companies if they hold onto inventories.

Irrespective of the single-value figure indicated by DSI, the company management should find a mutually beneficial balance between optimal inventory levels and market demand.

DSI vs. Inventory Turnover

A similar ratio related to DSI is inventory turnover, which refers to the number of times a company is able to sell or use its inventory over the course of a particular time period, such as quarterly or annually. Inventory turnover is calculated as the cost of goods sold divided by average inventory. It is linked to DSI via the following relationship:

Basically, DSI is an inverse of inventory turnover over a given period. Higher DSI means lower turnover and vice versa.

In general, the higher the inventory turnover ratio, the better it is for the company, as it indicates a greater generation of sales. A smaller inventory and the same amount of sales will also result in high inventory turnover. In some cases, if the demand for a product outweighs the inventory on hand, a company will see a loss in sales despite the high turnover ratio, thus confirming the importance of contextualizing these figures by comparing them against those of industry competitors.

DSI is the first part of the three-part cash conversion cycle (CCC), which represents the overall process of turning raw materials into realizable cash from sales. The other two stages are days sales outstanding (DSO) and days payable outstanding (DPO). While the DSO ratio measures how long it takes a company to receive payment on accounts receivable, the DPO value measures how long it takes a company to pay off its accounts payable. Overall, the CCC value attempts to measure the average duration of time for which each net input dollar (cash) is tied up in the production and sales process before it gets converted into cash received through sales made to customers.

Why the DSI Matters

Managing inventory levels is vital for most businesses, and it is especially important for retail companies or those selling physical goods. While the inventory turnover ratio is one of the best indicators of a company’s level of efficiency at turning over its inventory and generating sales from that inventory, the days sales of inventory ratio goes a step further by putting that figure into a daily context and providing a more accurate picture of the company’s inventory management and overall efficiency.

DSI and inventory turnover ratio can help investors to know whether a company can effectively manage its inventory when compared to competitors. A 2014 paper in Management Science, «Does Inventory Productivity Predict Future Stock Returns? A Retailing Industry Perspective,» suggests that stocks in companies with high inventory ratios tend to outperform industry averages. A stock that brings in a higher gross margin than predicted can give investors an edge over competitors due to the potential surprise factor. Conversely, a low inventory ratio may suggest overstocking, market or product deficiencies, or otherwise poorly managed inventory–signs that generally do not bode well for a company’s overall productivity and performance.

Example of DSI

These figures indicate that Walmart had a longer period of around 43 days to clear its inventory, while Microsoft took around 25 days.

days in inventory

Смотреть что такое «days in inventory» в других словарях:

Days in inventory — Days in inventory(DII) is an efficiency ratio that measures the average number of days the company holds its inventory before selling it. The formula for DII is: where the average inventory is the average of inventory levels at the beginning and… … Wikipedia

Days payable outstanding — (DPO) is an efficiency ratio that measures the average number of days a company takes to pay its suppliers. The formula for DPO is: where ending A/P is the accounts payable balance at the end of the accounting period being considered and COGS/day … Wikipedia

Days sales outstanding — In accountancy, Days Sales Outstanding (also called Days Receivables) is a calculation used by a company to estimate their average collection period. A low number of days indicates that the company collects its outstanding receivables quickly.… … Wikipedia

Inventory — means a list compiled for some formal purpose, such as the details of an estate going to probate, or the contents of a house let furnished. This remains the prime meaning in British English.[1] In the USA and Canada the term has developed from a… … Wikipedia

Inventory turnover ratio — is one of the Accounting Liquidity ratios, a financial ratio. This ratio measures the number of times, on average, the inventory is sold during the period. Its purpose is to measure the liquidity of the inventory. A popular variant of the… … Wikipedia

Inventory Turnover — A ratio showing how many times a company s inventory is sold and replaced over a period. the The days in the period can then be divided by the inventory turnover formula to calculate the days it takes to sell the inventory on hand or inventory… … Investment dictionary

days’ sales in inventory — The amount of inventory (stock) expressed in days of sales. For example, if 2 items a day are sold and 20 items are held in inventory, this represents 10 days (20/2) sales in inventory … Accounting dictionary

days inventory — The level of inventory expressed as its equivalent in days of a portion of cost of goods sold for the year. Calculated by multiplying inventory by 365 and then dividing that product by cost of goods sold. American Banker Glossary … Financial and business terms

Days’ sales in inventory ratio — The average number of days worth of sales that is held in inventory. The New York Times Financial Glossary … Financial and business terms

days’ sales in inventory ratio — The average number of days worth of sales that is held in inventory. Bloomberg Financial Dictionary … Financial and business terms

Days Inventory Outstanding

What is Days Inventory Outstanding (DIO)?

Days inventory outstanding (DIO) is the average number of days that a company holds its inventory Inventory Inventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a before selling it. The days inventory outstanding calculation shows how quickly a company can turn inventory into cash. It is a liquidity metric and also an indicator of a company’s operational and financial efficiency. Days inventory outstanding is also known as “inventory days of supply,” “days in inventory,” or “the inventory period.”

Days Inventory Outstanding Formula

The formula for days inventory outstanding is as follows:

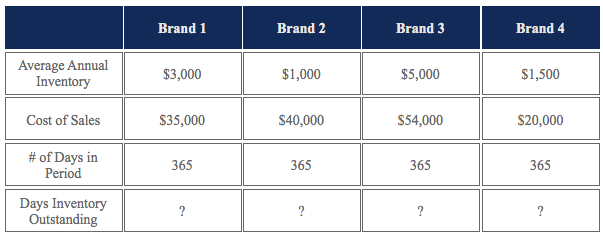

Days Inventory Outstanding = (Average inventory / Cost of sales) x Number of days in period

Example of Days Inventory Outstanding

Company A sells several brands of furniture. The manager would like to determine which brands are doing well in terms of inventory turnover. He’s tasked you with determining the days inventory outstanding for several different brands:

To determine the DIO of each brand:

From determining the DIO of each brand, you can easily see which brands are doing well relative to other brands. In this case, Brand 2 is doing extremely well, while Brands 1,3, and 4 are all lagging about equally behind. The manager may then meet with the sales and marketing team to try to figure out how to improve sales of those brands. The company might consider dropping Brand 3, the poorest performer, entirely.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Days Inventory Outstanding Template

Interpretation of Days Inventory Outstanding

A low days inventory outstanding indicates that a company is able to more quickly turn its inventory into sales. Therefore, a low DIO translates to an efficient business in terms of inventory management and sales performance.

A high days inventory outstanding indicates that a company is not able to quickly turn its inventory into sales. This can be due to poor sales performance or the purchase of too much inventory. Having too much idle inventory is detrimental to a company as inventory may eventually become obsolete and unsellable. Holding excess inventory also negatively impacts cash flow.

Importance of Days Inventory Outstanding

More Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)® Become a Certified Financial Modeling & Valuation Analyst (FMVA)® CFI’s Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

Free Accounting Courses

Learn accounting fundamentals and how to read financial statements with CFI’s free online accounting classes.

These courses will give the confidence you need to perform world-class financial analyst work. Start now!

Building confidence in your accounting skills is easy with CFI courses! Enroll now for FREE to start advancing your career!

days sales in inventory

Полезное

Смотреть что такое «days sales in inventory» в других словарях:

days’ sales in inventory — The amount of inventory (stock) expressed in days of sales. For example, if 2 items a day are sold and 20 items are held in inventory, this represents 10 days (20/2) sales in inventory … Accounting dictionary

Days’ sales in inventory ratio — The average number of days worth of sales that is held in inventory. The New York Times Financial Glossary … Financial and business terms

days’ sales in inventory ratio — The average number of days worth of sales that is held in inventory. Bloomberg Financial Dictionary … Financial and business terms

Объем запасов на продажу (DAYS SALES IN INVENTORY) — Показатель достаточности запасов. Рассчитывается делением остатка запасов на конец отчетного периода за вычетом всех резервов на среднюю ежедневную себестоимость реализации (или себестоимость использованных материалов при оценке запасов сырья) за … Словарь терминов по управленческому учету

Days sales outstanding — In accountancy, Days Sales Outstanding (also called Days Receivables) is a calculation used by a company to estimate their average collection period. A low number of days indicates that the company collects its outstanding receivables quickly.… … Wikipedia

Inventory — means a list compiled for some formal purpose, such as the details of an estate going to probate, or the contents of a house let furnished. This remains the prime meaning in British English.[1] In the USA and Canada the term has developed from a… … Wikipedia

Days in inventory — Days in inventory(DII) is an efficiency ratio that measures the average number of days the company holds its inventory before selling it. The formula for DII is: where the average inventory is the average of inventory levels at the beginning and… … Wikipedia

Days payable outstanding — (DPO) is an efficiency ratio that measures the average number of days a company takes to pay its suppliers. The formula for DPO is: where ending A/P is the accounts payable balance at the end of the accounting period being considered and COGS/day … Wikipedia

Sales (accounting) — In bookkeeping, accounting, and finance, Net sales are operating revenues earned by a company when it sells its products. Revenue (net sales) are reported directly on the income statement as Sales or Net sales. In financial ratios that use income … Wikipedia

Inventory Turnover — A ratio showing how many times a company s inventory is sold and replaced over a period. the The days in the period can then be divided by the inventory turnover formula to calculate the days it takes to sell the inventory on hand or inventory… … Investment dictionary