Unlevered Beta

:max_bytes(150000):strip_icc()/pic16-9b4adcd4fb7644e98174412f2c3fdebb.jpg)

:max_bytes(150000):strip_icc()/peter-de4f1081c5ff4dba884cf141c18963f3.jpg)

Peter Westfall is a professor of statistics at Texas Tech University. He has more than 30 years of statistics experience including teaching, research, writing, and consulting. Peter teaches and performs statistical research with a focus on advanced statistical methods, regression analysis, multivariate analysis, mathematical statistics, and data mining. He specializes in using statistics in investing, technical analysis, and trading.

:max_bytes(150000):strip_icc()/YariletPerez-d2289cb01c3c4f2aabf79ce6057e5078.jpg)

Yarilet Perez is an experienced multimedia journalist and fact-checker with a Master of Science in Journalism. She has worked in multiple cities covering breaking news, politics, education, and more. Her expertise is in personal finance and investing, and real estate.

Beta is a measure of market risk. Unlevered beta (or asset beta) measures the market risk of the company without the impact of debt.

‘Unlevering’ a beta removes the financial effects of leverage thus isolating the risk due solely to company assets. In other words, how much did the company’s equity contribute to its risk profile.

Key Takeaways

Unlevered Beta

Understanding Unlevered Beta

Beta is the slope of the coefficient for a stock regressed against a benchmark market index like the Standard & Poor’s (S&P) 500 Index. A key determinant of beta is leverage, which measures the level of a company’s debt to its equity. Levered beta measures the risk of a firm with debt and equity in its capital structure to the volatility of the market. The other type of beta is known as unlevered beta.

‘Unlevering’ the beta removes any beneficial or detrimental effects gained by adding debt to the firm’s capital structure. Comparing companies’ unlevered betas give an investor clarity on the composition of risk being assumed when purchasing the stock.

Take a company that is increasing its debt thus raising its debt-to-equity ratio. This will lead to a larger percentage of earnings being used to service that debt which will amplify investor uncertainty about future earnings stream. Consequently, the company’s stock is deemed to be getting riskier but that risk is not due to market risk.

Isolating and removing the debt component of overall risk results in unlevered beta.

The level of debt that a company has can affect its performance, making it more sensitive to changes in its stock price. Note that the company being analyzed has debt in its financial statements, but unlevered beta treats it like it has no debt by stripping any debt off the calculation. Since companies have different capital structures and levels of debt, an analyst can calculate the unlevered beta to effectively compare them against each other or against the market. This way, only the sensitivity of a firm’s assets (equity) to the market will be factored in.

To ‘unlever’ the beta, the levered beta for the company has to be known in addition to the company’s debt-equity ratio and corporate tax rate.

Systematic Risk and Beta

Systematic risk is the type of risk that is caused by factors beyond a company’s control. This type of risk cannot be diversified away. Examples of systematic risk include natural disasters, political elections, inflation, and wars. Beta is used to measure the level of systematic risk, or volatility, of a stock or portfolio.

Beta is a statistical measure that compares the volatility of the price of a stock against the volatility of the broader market. If the volatility of the stock, as measured by beta, is higher, the stock is considered risky. If the volatility of the stock is lower, the stock is said to have less risk.

A beta of one is equivalent to the risk of the broader market. That is, a company with a beta of one has the same systematic risk as the broader market. A beta of two means the company is twice as volatile as the overall market, but a beta of less than one means the company is less volatile and presents less risk than the broader market.

Example of Unlevered Beta

For example, calculating the unlevered beta for Tesla, Inc. (as of November 2017):

Unlevered beta is almost always equal to or lower than levered beta given that debt will most often be zero or positive. (In the rare occasions where a company’s debt component is negative, say a company is hoarding cash, then unlevered beta can potentially be higher than levered beta.)

If the unlevered beta is positive, investors will invest in the company’s stock when prices are expected to rise. A negative unlevered beta will prompt investors to invest in the stock when prices are expected to decline.

How Can Unlevered Beta Help an Investor?

Unlevered beta removes any beneficial or detrimental effects gained by adding debt to the firm’s capital structure. Comparing companies’ unlevered betas give an investor clarity on the composition of risk being assumed when purchasing the stock. Since companies have different capital structures and levels of debt, an investor can calculate the unlevered beta to effectively compare them against each other or against the market. This way, only the sensitivity of a firm’s assets (equity) to the market will be factored in.

What Is Beta?

Simply put, beta (ß) is a measure of market risk. More precisely, it is a measure of the volatility—or systematic risk—of a security or portfolio compared to the market as a whole. In statistical terms, it is the slope of the coefficient for a security (stock) regressed against a benchmark market index (S&P 500). Each of these data points represents an individual stock’s returns against those of the market as a whole. So, beta effectively describes the activity of a security’s returns as it responds to swings in the market.

What Is Levered Beta?

Levered beta measures the risk of a firm with debt and equity in its capital structure to the volatility of the market. A key determinant of beta is leverage, which measures the level of a company’s debt to its equity. So, a publicly traded security’s levered beta measures the sensitivity of that security’s tendency to perform in relation to the overall market. A levered beta greater than positive 1 or less than negative 1 means that it has greater volatility than the market. A levered beta between negative 1 and positive 1 has less volatility than the market.

Relevering Beta in WACC

We quite often use leverage to improve returns. When evaluating a business, it is important to assess underlying performance with as well as without the impact of leverage. To measure performance without the impact of capital structure, we need unlevered Beta or Asset Betas. This post will look at relevering Beta in WACC (weight average cost of capital).

1. Why do we need to relever Beta?

From a valuation perspective in a buyout opportunity there is quite often a dramatic change in capital structure, specially within Leveraged and Management Buy outs (MBOs and LBOs). Within this context, the current capital structure is not relevant to the buyer. Beta, therefore, first needs to be unlevered to get to Asset Beta. Then Asset Betas are re-levered again to test the impact of multiple debt levels (proposed capital structure) to find an optimal mix between risk, returns and debt pay down schedules.

When assessing the value of a company’s operation we discount free cash flows using the weighted average cost of capital (WACC). WACC or weighted average cost of capital is calculated using the cost of equity and cost of debt weighing them by respective proportions within the optimal or target capital structure of the company, i.e.

WACC = E/(D+E)*Cost of Equity + D/(D+E) * Cost of Debt, where E is the market value of equity, D is the market value of Debt.

The cost of debt can be observed from bond market yields. Cost of equity is estimated using the Capital Asset Pricing Model (CAPM) formula, specifically

Cost of Equity = Risk free Rate + Beta * Market Risk Premium

a. Risk components in levered Beta

Beta in the formula above is equity or levered beta which reflects the capital structure of the company. The levered beta has two components of risk, business risk and financial risk.

Business risk represents the uncertainty in the projection of the company’s cash flows which leads to uncertainty in its operating profit and subsequently uncertainty in its capital investment requirements.

Financial risk represents the additional risk placed on the common shareholders as a result of the company’s decision to use debt, i.e. financial leverage.

If capital structure comprised of 100% equity then beta would only reflect business risk. This beta would be unlevered as there is no debt in the capital structure. It is also known as asset beta.

2. How do we relever Beta in WACC?

To obtain the equity beta of a particular company, we start with a portfolio of assets of that company or alternatively a sample of publicly traded firms with similar systematic risk. We will first derive the betas of these individual assets or firms from market prices. The derived betas are levered betas as they would reflect the capital structure of the respective firms. They have to be unlevered so as to only reflect their business risk components.

From the unlevered betas, obtain a weighted average unlevered beta using as weights the proportions of the assets in the company’s asset portfolio or derive an average across all comparable firms. The weighted unlevered beta thus obtained would now be relevered based on the capital structure of the company in order to determine the equity or levered beta for the company. This beta would reflect not only the business risk but also the financial risk of the company.

a. Practitioner’s method vs Risky-debt formula

Unlevering and relevering beta in WACC may be done in a number of ways. A method employed by practitioners gives the relationship between unlevered and relevered beta as follows:

Levered Beta = Unlevered Beta * (1+D/E), where D/E = Debt-to-Equity Ratio of the company.

The practitioner’s method makes the assumption that corporate debt is risk free. If we consider corporate debt as risky then another possible formulation for relevering beta in WACC is:

Levered Beta = Asset Beta + (Asset Beta – Debt Beta) * (D/E) where we estimate Debt Beta from the risk free rate, bond yields and market risk premium.

b. Considering Taxation

The above formulations do not incorporate the impact of corporate taxation, i.e. the fact that debt returns tend to be tax deductible. In order to consider the impact of taxation the following adjustments will be made in the relationships given above:

Under the practitioner’s method:

Levered Beta = Unlevered Beta * (1+D*(1-T)/E) where T is the tax rate.

Under the risky-debt formulation:

Levered Beta = Asset Beta + (Asset Beta – Debt Beta) * (D/E)*(1-T).

And WACC would be equal to E/(D+E)*Cost of Equity + D*(1-T)/(D+E) * Cost of Debt.

c. Example

BetaCorp is a corporation that has two primary business lines – personal hygiene and consumer off the shelf pharmaceuticals. We are estimating its levered beta for the purpose of determining its cost of equity. The personal hygiene subsidiary is worth USD 20 million while the consumer pharma subsidiary is worth USD 30 million. The firm has a debt-to-equity ratio of 1. Assume that the tax rate for all firms is 30%. The risk free rate is 7% and the market risk premium is 6%. The following information is for firms with comparable systematic risk:

| Comparable Firms | Average Beta | Average D/E Ratio |

| Personal Hygiene | 0.9 | 20% |

| Medical | 1.2 | 60% |

Note that the average betas above denote the average of the levered or equity betas of these firms.

In the first step we will calculate the unlevered betas for each group of firms using the practitioner’s method:

Unlevered Beta for the personal hygiene business = 0.9 / (1+ 0.2*(1-0.3)) = 0.79

Unlevered Beta for the consumer pharma business = 1.2 / (1+ 0.6*(1-0.3)) = 0.85

The Beta for BetaCorp will be the weighted average of unlevered betas where the weights are in proportion to the subsidiaries value in the firm, i.e.

Unlevered Beta for BetaCorp = 0.79*20m/50m+0.85*30m/50m = 0.82

Levered Beta for BetaCorp = 0.82*(1+1*(1-0.3)) = 1.40

Cost of Equity = 7%+1.40*6% = 15.39%.

d. WACC, Beta and Market Risk Premium – Industry specific

We can extend the same model to calculate industry specific WACC estimates.

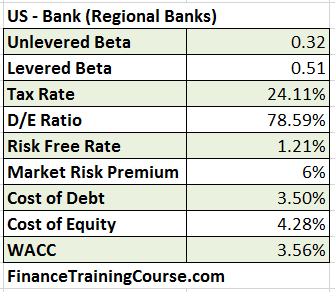

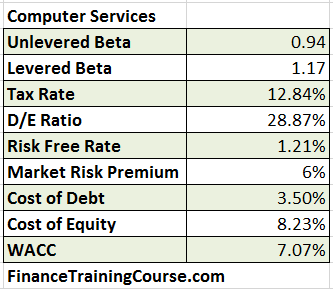

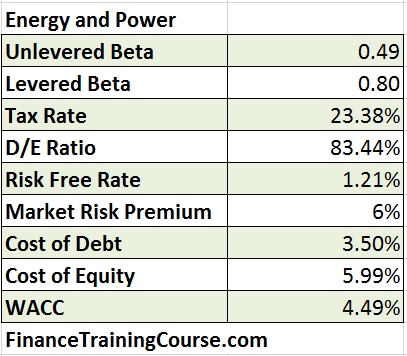

For instance, the figure below shows the calculation for US regional banks, the Computer Services industry and Energy and Power sector using the January 2016 data set shared by NYU and Dr. Damodran on their site.

i. Regional Banks

We have used the default 6% estimate (2015) for Market Risk Premium for all three industries.

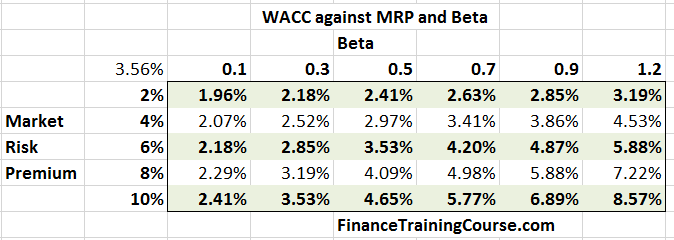

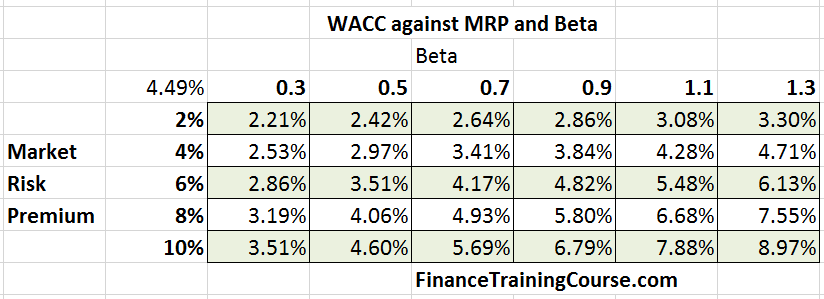

A quick sensitivity test of WACC by changing values of Beta and Market Risk Premium shows a range of WACC values between 1.96% – 8.57% for regional banks in the US. This range can become a third input in our in-class valuation intuition exercise

ii. Computer Services

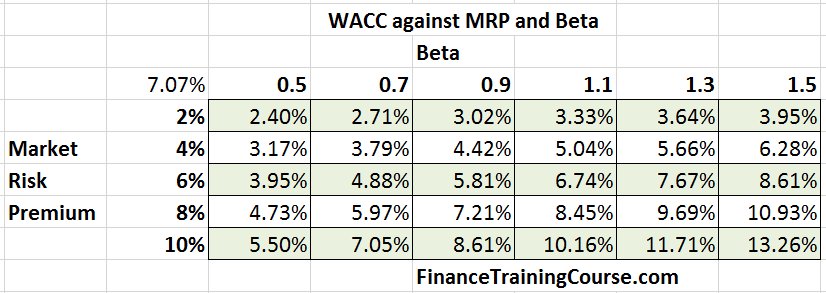

While we have used the same risk premium, different Beta and Leverage ratios lead to a different value of WACC for the Computer Services industry and the Energy and Power segment.

As expected a different WACC and a different relevant range because of change in WACC parameters.

iii. Energy & Power

WACC calculations for Energy and Power sector.

Sensitivity analysis for Energy and Power sector.

We can now use these estimates as part of our valuation exercises and case studies such as:

If you have an interest in using Beta and Alpha outside of the valuation and WACC world, such as in portfolio construction, portfolio allocation and portfolio optimization models see:

Чем выше значение беты, тем выше стоимость капитала, потому что повышенный риск для инвесторов (через повышенную чувствительность к колебаниям рынка) должен быть компенсирован за счет более высокой прибыли.

ВЫЧИСЛЕНИЕ ИСТОРИЧЕСКОГО ЗНАЧЕНИЯ КОЭФФИЦИЕНТА БЕТА

.png)

b x – коэффициент бета акции X

Cov (x, y) – ковариация между доходностями цены акции X и индекса акций Y

Var (y) – дисперсия доходности индекса акций Y

x – среднее арифметическое значение доходности акции

y – среднее арифметическое значение доходности индекса

n – количество наблюдений

UNLEVERED И LEVERED КОЭФФИЦИЕНТ БЕТА

β unlevered = β levered / [ 1 + ((1 – Ставка налога) * Долг/Капитал) ]

Пример. Рассчитаем β для применения в WACC при построении модели DCF. Допустим ставка налога в США составляет 20%. В приведенной ниже таблице указаны коэффициенты беты, найденные на основе исторических доходностей за последние 5 лет и средняя структура капитала каждой компании за последние 5 лет. Анализируемая компания финансируется за счет собственного капитала на 30 %, и долговых обязательств на 70 %.

Unlevered Beta

Unlevered Beta Definition

It is a risk measurement metric that compares the risk of a company without any debt to the risk of the market. In simple language, it is the beta of a company without considering the debt. It is also referred to as asset beta because the risk of a firm after removing leverage is because of its assets.

Levered Beta Vs. Unlevered Beta

Beta or levered beta is a measure of systematic risk of a firm in relation to the market. Systematic risk is the risk that affects the overall market. Beta does not take into account the unsystematic risk. Unsystematic risk is the risk that specifically affects a stock so it can be reduced by diversifying the portfolio.

Some industries or companies have a high level of debt on their balance sheet. This leverage makes their earnings volatile and investment in this company becomes risky. Levered beta considers the risk of leverage and its impact on the company’s performance. So, levered beta is not an ideal measure to compare two companies with different debt proportions. In such a scenario, you will have to remove the effect of debt by “unlevering” the beta. Unlevered beta will facilitate a better comparison for such companies than levered beta.

Formula for Unlevered Beta

Unlevered beta or asset beta can be found by removing the debt effect from the levered beta. The debt effect can be calculated by multiplying the debt to equity ratio with (1-tax) and adding 1 to that value. Dividing levered beta with this debt effect will give you unlevered beta.

Pure Play Method

The capital asset pricing model (CAPM) can be used for publicly listed companies. Finding beta of projects or companies that are not publicly listed is not possible through CAPM due to the lack of data. The pure play method is used in such cases. Unlevered and levered beta is used in this method to estimate the beta.

Formula of Pure Play Method

Calculation of Unlevered Beta with Example

Let’s take an example to understand how it is calculated.

Company X is a non-listed private company. Here are some details available to you:

| Description | Company X |

| Total Debt | $ 2 million |

| Total Equity | $ 5 Million |

| Debt to Equity ratio | 40% |

| Tax rate | 30% |

You want to find out the beta for Company X.

Time needed: 10 minutes.

Stepwise calculation of Unlevered Beta

Firstly, you need to find out a comparable company that is similar in nature to Company X. Also, the comparable company must be publicly listed so that its beta can be calculated. You found a Company A which is very similar in nature to Company X. Company A is operating in the same industry and it has the same product line and risk profile as Company X. So, you have collected the following data about the comparable company:

The second step is to calculate the beta of the comparable company. Here, Company A has a beta of 1.2. Now, you will have to unlever the beta of Company A. in simple language, you have to remove the effect of leverage from the beta of company A. By applying the formula, we find the unlevered beta value to be 0.91.

Unlevered Beta (βCompany A) = Levered Beta (βCompany A) / <1+(1-Tax)*(Debt/Equity)>

Unlevered Beta (βCompany A) = 1.2 / <1+(1-0.35)*(0.5)>= 0.91

The last step is to adjust Company A’s (comparable company) unlevered beta for the capital structure of Company X. We will assume the unlevered beta of Company A will be the same as Company X because they are similar in nature. By adjusting the unlevered beta of Company X for its leverage, we will find the beta of Company X to be 1.17.

Levered beta (βCompany X) = Unlevered Beta (Company X) * [1 + <(1- Tax) (Debt/Equity)>]

Levered beta (βCompany X) = 0.91 * [1+<1-0.3)(0.4)>] = 1.17

ВЛИЯНИЕ СТРУКТУРЫ КАПИТАЛА НА СТОИМОСТЬ БИЗНЕСА ПРИ СЛИЯНИИ И ПОГЛОЩЕНИИ

Полный текст:

Аннотация

В результате слияний и поглощений, как правило, происходят существенные изменения структуры капитала, поэтому задачей управления на этапе прогнозирования является корректная оценка влияния этих изменений на стоимость будущей компании. В рамках данной статьи приведены методы измерения влияния структуры капитала на стоимость компании в рамках разных подходов к оценке, наиболее детально описаны способы, применяемые в рамках доходного подхода. Приводится метод подсчета средневзвешенной стоимости капитала, на базе модели оценки долгосрочных активов (capital asset pricing model, CAPM), а также ограничения, связанные с применением данной модели. Выявляется необходимость корректировки прогнозируемой стоимости привлечения не только собственных, но и заемных средств.

Ключевые слова

Для цитирования:

Мартынова В.С. ВЛИЯНИЕ СТРУКТУРЫ КАПИТАЛА НА СТОИМОСТЬ БИЗНЕСА ПРИ СЛИЯНИИ И ПОГЛОЩЕНИИ. Стратегические решения и риск-менеджмент. 2011;(5):102-105. https://doi.org/10.17747/2078-8886-2011-5-102-105

For citation:

Martynova V.S. CAPITAL STRUCTURE IMPACT ON MARKET VALUE OF MERGING COMPANIES. Strategic decisions and risk management. 2011;(5):102-105. (In Russ.) https://doi.org/10.17747/2078-8886-2011-5-102-105

При проведении процедуры слияния и поглощения расчет рыночной стоимости компаний проводится еще на этапе планирования, прежде всего в целях определения эффективности их деятельности до и после объединения. Компания- инициатор сравнивает полученную разницу с затратами, необходимыми для проведения сделки. Здесь нужно отметить, что, судя по данным рынка, только незначительное количество сделок приобретения компаний экономически выгодны. Например, в 1995 году журнал Business Week сообщил, что из 150 отобранных для исследования примеров слияний и приобретений в 1990-1995 годах только половина принесла доход акционерам приобретающих фирм. Исследование 700 слияний и приобретений в 1996-1998 годах, проведенное компанией KPMG, показало, что более 80% сделок не привели к увеличению стоимости объединенной компании по сравнению с суммарной стоимостью исходных компаний, а 50% привели к ее снижению [7, с. 13].

Даже при очевидном положительном эффекте от объединения (например, при распространении на всю организацию льгот, относившихся ранее только к компании-цели, сокращении управленческого аппарата, снижении издержек по операциям внутри компании) компания-инициатор может не достичь запланированных целей. К числу причин принадлежат как те, что относятся к прогнозу деятельности единой компании, так и те, которые имеют отношение к оценке компании- цели до слияния, а также технические причины (см. таблицу). Проблемы, указанные в первых двух столбцах таблицы и влекущие за собой большую часть различных возможных ошибок, так или иначе касаются процесса оценки стоимости компаний.

Исследование влияния доли заемных средств на стоимость компаний, особенно если речь идет о компаниях капиталоемких отраслей, является актуальным, так как на протяжении трех последних лет доступность финансирования значительно варьировала и не позволяла сделать прогноз как в плане макроэкономики, так и в плане отдельных ее сегментов.

С одной стороны, в случае привлечения заемного капитала для финансирования развития компаний (наращивания активов и доходов от их использования) влияние, оказываемое на денежные потоки, финансовый результат и величину активов, будет выше, чем размер платы за привлечение средств. Иными словами, отдача от вложений (рентабельность) должна быть выше, чем затраты на привлечение займов (процент). Кроме того, стоимость привлечения сравнивается с возникающим эффектом налогового щита. Таким образом, стоимость компании растет благодаря привлечению средств.

С другой стороны, привлечение заемного капитала ведет к большей вероятности ухудшения финансовой устойчивости организации, что, в свою очередь, повышает риски, связанные с вложениями и, как следствие, затраты на привлечение средств. Рост этих затрат ведет к снижению стоимости компании.

Необходимо отметить, что в оценке бизнеса влияние структуры капитала учитывается и при использовании затратного подхода (метода чистых активов): обязательства переоцениваются и вычитаются из суммы активов, а также в рамках сравнительного подхода (метода рынка капитала). Доля заемного капитала учитывается в составе тех показателей деятельности компании, к которым применяются мультипликаторы, а также при корректировке самих мультипликаторов (например, при наличии льгот у одной из компаний-аналогов). При применении мультипликатора «Цена/Выручка» рыночная стоимость заемных средств вычитается из результата, полученного для всего инвестированного капитала.

Наиболее распространенными формами привлечения заемного капитала являются:

Причины возникновения возможных ошибок при проведении слияний и поглощений

Проблема оценки стоимости компании-цели

Переоценка результатов синергизма расходов и доходов

Переоценка перспектив роста приобретаемой компании (рынка)

Неспособность эффективно интегрировать приобретаемую компанию после успешного слияния

Неспособность адекватно определить операционные и финансовые риски, связанные с компанией-целью

Риски, присущие вложениям в собственный капитал, учитываются при помощи ставки дисконтирования для собственного капитала, определяемой формулой модели оценки долгосрочных активов (capital asset pricing model, CAPM) или способом кумулятивного построения. Рассчитываемую ставку дисконтирования по модели CAPM находят по формуле

Расчет коэффициента бета с учетом соотношения долга и собственного капитала оцениваемой компании (relevered beta) осуществляется по формуле

Введение первого допущения может привести к неточности расчетов в связи с особенностями поведения игроков на фондовых рынках. Здесь нужно принять во внимание то, что для принятия решений о покупке или продаже акций используется как фундаментальный, так и технический анализ.

Фундаментальный анализ применяется инвесторами для оценки стоимости компании (или ее акций), которая отражает состояние дел в компании, рентабельность ее деятельности. При этом анализу подвергаются финансовые показатели компании: выручка, EBITDA (Eamings Before Interests Tax, Depreciation and Amortization), чистая прибыль, чистая стоимость компании, обязательства, денежный поток, величина выплачиваемых дивидендов и производственные показатели компании. Задачей фундаментального анализа является определение «истинной» цены исследуемых бумаг. Сравнивая полученную оценку с текущим состоянием рынка, делают вывод о переоцененно- сти либо недооцененности бумаг

К наиболее распространенным индикаторам, используемым для определения тенденций и поведения цен в ближайшем будущем, относятся:

Ни один из указанных индикаторов не учитывает индивидуальных особенностей компаний. Данные для расчета коэффициента бета аккумулируются по результатам торгов на фондовых рынках, следовательно, частично изменения происходят под влиянием колебаний в отрасли в целом и не отражают положения дел в компании в целом и соотношения собственного и заемного капитала в частности. Насколько существенна эта часть или, другими словами, какая доля инвесторов ориентируется на технический анализ рынков, точно сказать невозможно, однако фондовый рынок РФ относится к наиболее спекулятивным.

В целом правомерность применения коэффициента бета была подвергнута критике Ю. Фама и К. Френчем в 1980-х годах на основе эмпирически полученных данных об отсутствии пропорциональной зависимости доходности от величины коэффициента бета [3, с. 255]. Также была выявлена обратно пропорциональная зависимость доходности акций и размера компании, выраженного через капитализацию ее акций.

Техническая сложность расчета коэффициента бета связана с возможными существенными отклонениями структуры капитала отдельной компании-аналога от нормативных для отрасли в заданный период времени. В то же время компании, выбираемые для расчета среднеотраслевых показателей, могут быть крайне неоднородными и не подходящими для расчета уровня риска, характерного для оцениваемой организации.

В сообществе финансистов, специализирующихся на оценке компаний, проводится исследование альтернативных методов подсчета справедливой доходности. При расчете суммы рисков при помощи кумулятивного метода к безрисковой ставке процента по вложениям и рискам, присущим отрасли, добавляются следующие слагаемые, связанные непосредственно с деятельностью компании:

В частности, последний пункт прямо рассчитывается в зависимости от доли заемных средств на балансе. При этом, как правило, учитывается то, что в связи с финансовым кризисом и массовым снижением объемов кредитования значительно затрудняется доступ к капиталу, особенно для компаний, имеющих неблагоприятные показатели ликвидности и финансовой устойчивости.

К показателям, наиболее информативным с точки зрения потенциальных заемщиков, относятся:

Негативные результаты по какому-либо из указанных коэффициентов приводят к росту риска кредитования для займодателя и, как следствие, к росту риска, связанного с доступностью привлечения финансов в рамках метода кумулятивного построения [5, с. 33].

Таким образом, при проведении оценки с помощью доходного подхода при определении ставки дисконтирования предлагается пересмотреть риск, связанный с доступностью капитала, и возможную ставку привлечения заемного капитала при существенных изменениях структуры пассивов. В частности, если компания планирует рефинансирование долгов, наряду с изменениями структуры капитала необходимо откорректировать стоимость привлечения заемных средств с учетом приведенных выше критериев. При слиянии и поглощении существенные изменения структуры капитала могут быть связаны в первую очередь с формой финансирования самой сделки присоединения.

Список литературы

1. Брейли Р., Майерс С. Принципы корпоративных финансов. 2-е изд. М.: Олимп-Бизнес, 2004. 977 с.

2. ЗАО «Новое качество»: Электронный ресурс. Режим доступа: http://www.elitehome.ru.

3. Коупленд Т., Коллер Т., Муррин Дж. Стоимость компаний. 3-е изд. М.: Олимп-Бизнес, 2008. 554 с.

4. Найман Э. Л. Трейдер-Инвестор. Киев: ВИРА-Р, 2000. 640 с.

5. Павловец В. Какая кредитная нагрузка будет оптимальна для компании // Финансовый директор. 2010. №7–8(96). Июль-август. С. 29–35.

6. Рекомендации по подготовке финансовой модели // Внешэкономбанк: Электронный ресурс. Режим доступа: http://www.veb.ru/common/upload/files/veb/invest/rec1.pdf.

7. Феррис К., Пети Б. Оценка стоимости компании: как избежать ошибок при приобретении. М.: Вильямс, 2005. 255 с.

Об авторе

выпускник и аспирант. Работает в сфере оценки собственности с 2004 года.