LiveInternetLiveInternet

—Цитатник

Вам не хочется, или некогда, долго варить холодец. А может быть, ради небольшого лотка прос.

Люди с одинаковыми именами имеют не только сходные привычки, характеры, предпочтения и спосо.

Взяв на вооружение эти советы вы будете тратить времени в 2 раза меньше. Как убрать налеты на.

К сожалению, даже объединенные усилия граммар-наци не всем помогают запомнить.

—Видео

—Метки

—Рубрики

—Приложения

—Новости

—Поиск по дневнику

—Подписка по e-mail

—Друзья

—Постоянные читатели

—Сообщества

—Статистика

Brexit, Deutsche Bank — exit! Когда начнётся экономический развал ЕС?

Кто будет стоять за уничтожением Deutsche Bank?

При этом, несомненно, сама Британия понесла значительные издержки из-за своего решения. Так, по расчетам Центра экономических показателей при Лондонской школе экономики, в долгосрочной перспективе снижение объёмов торговли с ЕС обойдётся Великобритании в 9,5% ВВП, а спад объёмов иностранных инвестиций — в 3,4% ВВП или даже больше. Одни только эти потери уже намного превышают весь потенциальный выигрыш от Brexit’а. Чистый взнос Британии в бюджет ЕС в прошлом году составил всего лишь 0,35% ВВП. При этом выгода от отмены европейских норм регулирования будет невелика, поскольку трудовой и товарный рынки в стране уже и так едва ли не самые свободные в мире.

Инициатива будет в руках Евросоюза, который, можно не сомневаться, будет очень жестко вести себя с Британией. Многие участники экономической деятельности — немецкие автопроизводители, французские фермеры, финансовые центры Европы — захотят изолировать своих британских конкурентов. Со своей стороны, правительства стран ЕС захотят наказать Британию, и не в последнюю очередь потому, что они понимают, как бархатный развод с Британией способствует подъёму антиевропейских партий, таких как ультраправый Национальный фронт во Франции, уже призвавший к проведению референдума о членстве страны в ЕС.

В целом, согласно оценкам экспертов, в частности, немецкого фонда Бертельсмана, потери Великобритании из-за выхода из ЕС превысят до 2030 года 300 млрд евро, то есть, больше, чем по 20 млрд. евро в год. Тем не менее, несмотря на все эти потери, Лондон, для приличия прикрывшись мнением народа с целью избежать обвинений в развале ЕС, пошел на этот шаг. Почему?

Понять долгосрочную стратегию Лондона поможет другое событие — 15 января 2016 года Центробанк Швейцарии принял решение отвязать франк от евро. В результате, как отметил постоянный автор ИА REGNUM Александр Запольскис, ЦБШ сократил ЗВР Швейцарии примерно на 100−110 млрд. франков разом: «Самое время еще вспомнить об активах коммерческих швейцарских банков, у которых около 1,36 трлн. франков также номинированы в иностранной валюте. Хотя более-менее точные цифры одних только прямых потерь еще предстоит подсчитать, уже сейчас можно констатировать, что Швейцария своим этим решением одномоментно выбросила на ветер не менее 450−500 млрд. швейцарских франков или примерно 415 млрд. евро. За один день».

Возникает логичный вопрос — почему страна, на протяжении многих лет имеющая стабильный бюджетный профицит и резервы, в полтора раза превосходящие национальный ВВП (лучший показатель в мире!),пошла на столь разрушительный шаг для собственной экономики?

Ответ, по мнению Александра Запольскиса, состоит в том, что в начале января швейцарские банкиры узнали нечто такое, что делает все перечисленные потери совершенно обоснованными: «Вероятно, из серии — лучше сейчас потерять часть, чем потом потерять все. А так как речь с самого начала шла исключительно о курсе франка к евро, напрашиваются совершенно однозначные выводы. «Что-то такое» CNB выяснил на счет ближайшего будущего евро как мировой валюты. Если предположить, на минуту, что евро катастрофически обваливается, то привязанный к нему франк единая европейская валюта автоматически тянет за собой. На всю глубину своего падения.

Швейцария, конечно, богатая и даже индустриальная страна, но, не забываем, что в масштабе мировой экономики — это капля в море. Какие-то там 600 млрд. долл. ВВП Швейцарии ничего не сможет поделать против 15.669 млрд. всего Евросоюза. Напрашивается единственный вывод, который не противоречит всему произошедшему. Уже не столь важно, по какой причине — из-за риска выхода Греции из зоны евро, или в виду предстоящих планов ЕЦБ на счет QE, сам евро ждет чрезвычайно серьезный кризис. Причем, очень скоро. Он настолько близок, что времени на разработку хитрых маневров и обходных планов попросту не осталось. Швейцарские банковские профи решили соскочить. Для того они в первую очередь и отвязали швейцарский франк от европейской валюты. Не считаясь при этом ни с какими потерями. Масштаб потерь, на которые они уже откровенно махнули рукой, позволяет судить о размерах того бедствия, которое надвигается на Европу».

То есть как мы видим, сначала был вовсе не Brexit, а Schweizxit — в плане отвязки курса швейцарского франка от евро, на поддержание которого Швейцария тратила по 200 млрд. евро в год. И Берн точно также как, как и позднее Лондон, решился пойти на очень серьезные потери с целью избежать глобальных потерь в дальнейшем. Можно, конечно, говорить, что «одно совпадение — случайность, два — тенденция, а три — закономерность», но даже в этом случае — сначала Швейцария, потом — Британия, две отнюдь не последние страны в мировом политическом и экономическом рейтинге, мы уже имеем, как минимум, тенденцию, а третий случай, скорее всего, в данном контексте и станет отправной точкой к развалу ЕС или, как минимум, зоны евро.

Я при этом не упоминаю десятков примеров новой экономической реальности по мелочи, например, о сотнях танкеров, которые сейчас используются не по прямому назначению доставки нефти потребителям, а для ее хранения, или, например, произошедшей в начале июля заморозке вывода средств британскими фондами недвижимости — все их просто невозможности привести в рамках одной статьи.

По итогам 2015 года Deutsche Bank понёс убытков на сумму 6,8 миллиарда долларов. В первом квартале 2016 года (по оценкам самого банка и внешних экспертов) также ожидаются убытки. Как официально заявляют чиновники банка «волатильность рынков виновата». Акции Deutsche Bank упали до тридцатилетнего минимума, потеряв с начала года свыше 40% стоимости. Почему такое стало возможным?

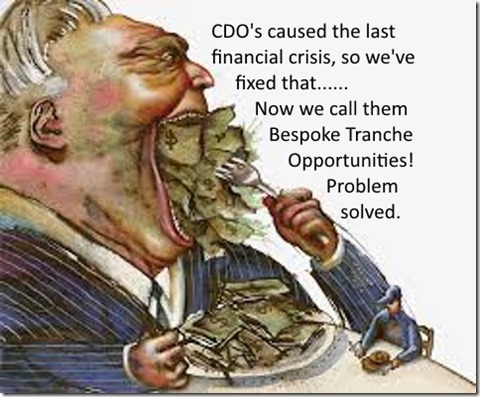

Дело в том, как отметил еще в марте 2016 года Александр Роджерс, что «после кризиса 2008 года несколько лет нигде в мире не рисковали снова затевать игры с CDO. Однако в 2013 году именно Deutsche Bank первым запустил их снова в оборот, только уже под новым названием bespoke tranche opportunity (дословно переводится как «сшитая на заказ по частям возможность»). Затем за ним, в погоне за высокими прибылями и с целью замаскировать токсичные активы на своих балансах, в эту игру снова включились и другие. Поэтому можно предположить с высокой вероятностью, что триггером нового витка кризиса послужит обрушение одного из участвующих в этой афёре банков — Deutsche Bank, BNP Paribas, JP Morgan или Citigroup. Ведь после 2008 года никто из их руководства не был наказан за создание пузыря, и теперь они надули новый, ещё больший»).https://www.imperiyanews.ru/details/c6458235-fa97−4d0d-9953-eeb83321b877

То есть Deutsche Bank стал играть в ту игру, за которую был наказан Lehman Brothers. В этой связи возникает два логичных вопроса. Первый — почему Deutsche Bank стал играть в эту игру, которая может обрушить не только экономику Германии и Евросоюза, но и уничтожить роль Германии как политического центра Европы? Второй — под чьим реальным управлением находится банк, формально находящийся в зоне немецкой юрисдикции?

В конце июня на проблемы Deutsche Bank обратил внимание в своем очередном докладе и МВФ, который заявил, что «Deutsche Bank является одним из глобальных системно значимых банков, который потенциально может нанести ощутимый вред финансовой системе на мировом уровне». Также в число самых проблемных банков вошли британский HSBC и швейцарский Credit Suisse» (оба входят в список крупнейших банков мира).

Главная проблема банка состоит в том, что по каким-то причинам последние месяцы и годы он стремительно наращивал на своем балансе число токсичных активов (в основном деривативов),которая на сегодня вылилась в пирамиду величиной около 75 трлн. евро (!),то есть сопоставима с масштабами всей мировой экономики.

«Если, а вернее КОГДА она обвалится, то падение Lehman Brothers покажется лёгким насморком по сравнению с бубонной чумой. Если падение Lehman Brothers в 2008 году привело к потере полутора миллионов рабочих мест только в одних США, выселению свыше 3 миллионов человек из их жилищ, падению объёмов мировой торговли, а последствия кризиса полностью не купированы до сих пор, невзирая на несколько серий «количественного смягчения» (QE) со стороны ФРС, то последствия нового кризиса, который может быть спровоцирован падением Deutsche Bank, будут в несколько раз плачевнее.

Даже аналитики МВФ признают, что оно вызовет цепную реакцию, которая обрушит не только еврозону, но и выльется на американские фондовые рынки. ЕЦБ самостоятельно не вытянет последствий подобного краха, а нежелание нести на себе всю тяжесть последствий (особенно после британского референдума о выходе из ЕС) подтолкнёт страны-участники к параду суверенитетов, в результате чего Евросоюз, скорее всего, прекратит своё существование.

И день, когда Deutsche Bank обанкротится, стремительно приближается. На последней торговой сессии в пятницу акции компании просели на 15%, установив новый исторический минимум. Ещё две-три такие сессии, и все. Вот и «Вести Финанс» удивляются, почему «история с Deutsche Bank по каким-то причинам долгое время не раскручивалась СМИ слишком сильно», хотя мы неоднократно писали о проблемах в этом банке ещё год назад (нас при этом по привычке называли паникёрами). Для наглядности сравните графики падения стоимости акций Deutsche Bank и Lehman Brothers. Как видим, они отображают почти идентичные тенденции. На самом деле аналогичные проблемы есть и у BNP Paribas, JP Morgan, Citigroup и ещё нескольких банков. Но, судя по тому, как внимание общественности сосредотачивают именно на DB, то принято решение реализовывать стратегию «Умри ты сегодня, а я завтра».

Однако, несмотря на все эти казусы и Brexit’ы, инвесторы по всему миру видят не падение рынков, а их рост на 10%. И это вызывает закономерный вопрос — «кто же тащит рынки вверх, когда они должны уже давным-давно быть внизу?» Иван Колыхалов дает следующий ответ:«На графике мы видим общие покупки активов центральными банками (где BoJ — Банк Японии, Fed — Федрезерв, ECB — Европейский Центральный Банк, EM — банки развивающихся стран, SNB — Национальный банк Швейцарии). Так кто же агрессивно скупает всё, когда все остальные продают? ЕЦБ и Банк Японии (красная и голубая зона на графике). Зачем им это нужно? Почему оба банка так агрессивно выпускают всё больше ликвидности в рынок, путем объявления всё больших программ QE (количественных смягчений),поднимая цены на активы всё к большим высотам?»).

То есть, вторую волну кризиса изо всех сил сдерживают Европейский Центробанк и Банк Японии. Из этого следует, что Япония и зона евро находятся под самым сильным ударом от грядущего финансового кризиса. Но как нам демонстрирует вся история человечества, еще ни разу не было случая, чтобы перезапуск мировой системы происходил без войны. Поэтому и тащит мировая «партия войны» изо всех сил к власти в США психически неуравновешенную Хиллари Клинтон, чтобы иметь на этом месте человека, который при необходимости без колебаний обнулит долги Запада перед мировым сообществом.

Как отмечает Иван Колыхалов, «в прошлой статье я предположил, что именно Brexit станет той искрой, что взорвет рынки. Отчасти оно так и случилось, однако я не смог предположить, какой массовый влив ликвидности будет оказывать ЕЦБ и Банк Японии на рынки. Очевидно, что рынки спасают всеми возможными способами, все сваливания мгновенно откупаются, центробанки всеми силами пытаются удержать стоимость активов на плаву, иначе крупнейшие банки один за другим начнут схлопываться, как Lehman Brothers. ЕЦБ и Банк Японии в панике ‑ и используют все возможные манипуляции.

Федрезерв в 2016 году прекратил последнюю программу количественного смягчения (попросту: выпуск новых денег) и единственное, что может удерживать рынки на плаву — это только прибыли корпораций. Но последние два месяца приносят лишь новости о массовом сокращении прибылей во всех топовых корпорациях, на которых держатся индексы, индекс цен производителей (Industrial PMI),а также индекс промышленного производства (US industrial production) снижаются уже 9 месяцев подряд вместо роста. Сейчас достаточно одного резкого шока для того, чтобы пороховой склад взлетел на воздух.

Here’s Why ‘The Big Short’s Ending Matters

When something’s reputation either fizzles or completely goes south, it makes sense to rebrand. It’s a strategy that clothing lines, restaurants, and Snoop Lion (Dogg?) have all utilized. And yes, banks deployed this tactic following the 2008 financial crisis, renaming the high-risk investment packages that contributed to the collapse of the American economy. At the end of the Oscar-nominated film The Big Short, viewers were warned that little has changed, and these new (but essentially the same) investments would lead to a similar financial catastrophe. But should The Big Short’s warning of another financial crisis be taken seriously? Bustle talked to a couple of financial experts to find out.

For those who haven’t seen it, the film aims to explain the complicated financial crisis of 2007-2008 from the point of view of four groups of finance guys who predicted and then correctly bet on the collapse of the credit and housing markets. At the heart of the problem were collateralized debt obligations (CDOs), packages of mortgage loans that were legally put together by banks and sold to investors, who jumped at the chance for high returns. As demand for CDOs grew, banks began issuing bad (aka subprime) mortgage loans, which are extremely risky because there’s a greater chance that borrowers won’t be able to pay them off. Riskier homeowners inevitably couldn’t pay their mortgages and defaulted on their houses, leading to way more supply than demand in the housing market and causing it to crash.

As you might expect, people weren’t clamoring to buy CDOs after they lost trillions of dollars less than a decade ago, so banks changed them slightly and then stuck a new name on the packages: «bespoke tranche opportunities» (BTOs). Whereas CDOs broke a pool of mortgages into categories based on their riskiness and sold different layers to different investors, BTOs are made up of loans chosen to meet specific investors’ needs. Similarly to a bespoke suit, BTOs are one-of-a-kind, customized for the client. But despite this difference, BTOs still rely on banks and investors to take dangerous risks for higher returns.

«You can try to address some of the problems that led to blowups in CDOs before, but I think some of the underlying economics persist,» Craig Pirrong, professor of finance at the University of Houston’s Bauer College of Business, tells Bustle. «There are still incentives for the banks and investors creating and buying these packages (namely, making a lot of money), while the entities issuing loans to prospective homeowners don’t have much reason to adequately evaluate the risks. Since those issuing loans plan to sell them off, they rid themselves of any financial consequences should homeowners default and the cash flow dry up.»

The financial crisis of 2008 really spiraled when the housing market collapsed, and BTOs are vulnerable to similar situations, should they arise. «The way these things are structured and designed means they’re more susceptible to economy-wide risks,» Pirrong tells Bustle.

What’s keeping BTOs from causing the same major problems as CDOs, then? «There is a different regulatory environment that potentially will restrain the growth of these products,» Pirrong says. The main addition is the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank for short). Simply put, the legislation passed in 2010 created oversight councils that regulate the riskiest transactions, look for elements that could affect the whole financial market, protect consumers, and forbid banks from owning, investing, or sponsoring hedge funds, private equity funds, or any proprietary trading operations for their own profit.

Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania, tells Bustle that Dodd-Frank can’t definitively prevent another catastrophe, but it will certainly make a repeat of history less likely.

On top of the new legal protections, BTOs are not nearly as common as CDOs were in the years leading up to 2008 (at least, not yet), which makes it even less probable that the investments will all go south. Of course, there are still risky transactions happening, as the finance industry often thrives on betting money in order to make a lot more, but they aren’t affecting the market in the same way. «Yes, there are deals that raise eyebrows, but its not going to bring the market down,» Wachter says.

It’s always possible for widespread risky financial behavior to severely cripple the economy and cause a disaster similar to the last one. «If — through another mechanism — you would have widespread poorly underwritten lending, then sure, it could happen again,» Wachter tells Bustle. However, BTOs probably won’t do that in their current state.

Pirrong warns that just because BTOs aren’t a problem now doesn’t mean they never will be. The Big Short’s prediction was based on very real circumstances, but was a bit preemptive. «This is something to keep our eyes on, but it’s not necessarily a looming threat,» Pirrong says. «It’s worth watching.»

Credit Default Swaps Return with the Bespoke Tranche Opportunity

“Credit Default Swaps.”

“Collaterlized Debt Obligations.”

These are words and phrases I’d hoped to never see again.

These nasty little words – along with other gems like “subprime mortgages,” «derivatives,» and “asset-backed securities” – are what formed the nexus for the great financial crisis of 2008.

I had just started my career in financial publishing right around that time, almost a decade ago. And so it was my job for the next three years, to analyze, break down, and explain exactly how everything went to shit.

It has been a while, so if you need a refresher.

For years, investment banks put together packages (CDOs) made up of thousands of mortgage loans (tranches). The banks then sold them to buyers that were attracted by the high yields.

Of course, the banks didn’t mention that the yields were high because the investments were beyond risky, or that they were betting against them.

Good home loans were bundled together with subprime mortgages. And as homeowners failed to pay their mortgages, the value of the CDOs collapsed. The collapse caused a massive shockwave that toppled not just the U.S., but the global economy.

You’d think the resultant chaos would have taught us a lesson. but it didn’t.

After getting your report, you’ll begin receiving the Outsider Club e-Letter, delivered to your inbox daily.

Financial regulations that would prevent a replay of this disaster were blocked by hedge-fund lobbyists and abandoned by corrupt politicians.

And collaterlize debt obligations have returned under a new name: bespoke tranche opportunities.

A bespoke tranche opportunity is essentially a CDO backed by credit default swaps. They’re pools of derivatives that are cut into varying slices of risk and sold to investors.

“A tranche of a bespoke portfolio of credits can offer exposure to diversified risk with the possibility of leverage, credit enhancement and enhanced returns,” according to an e-mail from a Goldman Sachs employee, reviewed by Bloomberg News. It went out with the header: “Goldman: BESPOKE TRANCHE OPPORTUNITY.”

I don’t know about you, but that sure has a familiar ring to me.

I can’t say I’m surprised investors, like moths to a flame, are once-again being lured into risky, high-yielding “enhanced returns.”

Yield is hard to come by after six years of near-zero interest rates from the Federal Reserve.

Still, I thought we’d all learned our lesson in 2008.

This, sadly, won’t be the last time I write about CDOs, CDSs, tranches, or subprime lending.

I only have myself to blame, I guess. This is the life I’ve chosen.

Jason Simpkins is Assistant Managing Editor of the Outsider Club and Investment Director of Wall Street’s Proving Ground, a financial advisory focused on security companies and defense contractors. For more on Jason, check out his editor’s page.

*Follow Outsider Club on Facebook and Twitter.

You’ll Never Be On the Inside!

After getting your report, you’ll begin receiving the Outsider Club e-Letter, delivered to your inbox daily.

Coronavirus is causing tremendous panic leading to a shakeup in global markets. But rather than panic from the pandemic, you can profit.

In our latest report, «Superbugs and Your Wallet: 3 Ways to Inoculate Your Portfolio» we discuss the various ways people are duped by certain health care stocks and offer much more legitimate options and strategies.

We even include the 3 best stocks to repair your portfolio in dire times like these. Become an Outsider today, and receive this report FREE!

Tag Archives: Bespoke Tranche Opportunities

From CDO’s to BTO’s: Wall St. tees up the next financial disaster

Think Progress picked up on a piece from Bloomberg News which ought to be raising eyebrows on Main Street. The banksters are at it again, only this time those pesky Credit Default Obligations which brought down our financial system in 2007-2008 have been repackaged and served up under a new label: Bespoke Tranche Opportunities.

As the Think Progress analysis reports, these derivatives were an extremely important part of the last mess:

Now, we can move on to what makes these BTO’s a problem, beginning with their creation:

“The new “bespoke” version of the idea flips that (CDO) business dynamic around. An investor tells a bank what specific mixture of derivatives bets it wants to make, and the bank builds a customized product with just one tranche that meets the investor’s needs. Like a bespoke suit, the products are tailored to fit precisely, and only one copy is ever produced.” [TP]

Now, why would anyone want to buy one of these products, much less order a special one? In the Bad Old Days fund managers could choose to purchase some tranched up CDO, those blew up, so why go out and order one tailored to their specifications? Let’s return to the Bloomberg article:

“Goldman Sachs Group Inc. is joining other banks in peddling something they’re referring to as a “bespoke tranche opportunity.” That’s essentially a CDO backed by single-name credit-default swaps, customized based on investors’ wishes. The pools of derivatives are cut into varying slices of risk that are sold to investors such as hedge funds.

The derivatives are similar to a product that became popular during the last credit boom and exacerbated losses when markets seized up. Demand for this sort of exotica is returning now and there’s no real surprise why. Everyone is searching for yield after more than six years of near-zero interest rates from the Federal Reserve, not to mention stimulus efforts by central banks in Japan and Europe.” (emphasis added)

Translation: Because interest rates have been kept low by central banks hoping to keep struggling economies moving ahead, banks haven’t been able to make what they deem to be enough profit off corporate and Treasury bonds, and therefore have started playing in the “financial product” game again (not that they ever really stopped for long) and have started making ‘bets’ (derivatives) in the Wall Street Casino – with ‘products’ (BTO’s) which aren’t subject to the reforms put in place by the Dodd Frank Act.

So, what’s the problem? A hedge fund manager wants to buy a structured financial product from a bank which has a higher yield than what he can get by investing in corporate bonds or Treasuries… what could go wrong? Let us count the ways.

#1. These securities aren’t tied to the performance of the real economy as corporate bonds would be. In the jargon du jour, the BTO portfolio is a table of reference securities. Here come the Quants again, there are formulas for determining the ‘value’ of these securities which may or may not be valid, and they certainly weren’t during the Housing Bubble.

#3. The BTO encourages the same Wall Street Casino behavior we saw in the last Housing Bubble/Derivatives Debacle. It’s explained this way:

“The trouble with this game is that the value of most structured finance products is opaque and subject to sharp and violent change under conditions of financial stress. So when they are “funded” in carry-trade manner via repo or other prime broker hypothecation arrangements, the hedge-fund gamblers who have loaded up on these newly minted structures are subject to margin calls which can spiral rapidly in a financial crisis. And that, in turn, begets position liquidation, plummeting prices for the “asset” in question, and even more liquidation in a downward spiral.” [WolfStreet]

Sound familiar? Sound a bit like Lehman Brothers? Remove the jargon and the message is all too familiar – no one really knows the value of the structured product, and if the product is purchased with borrowed funds it’s subject to margin calls (people wanting their money back) which in turn leads to sell offs and the price for the “thing” drops off the financial cliff, and…. down we go. Again. We’ve seen this movie before, and the ending wasn’t pleasant.

#4. The BTO is a way around financial reform regulations. The offerings, be they FIGSCO or BTO’s are being peddled at the same time the Financialists are trying their dead level best to (a) get Congress to whittle down the regulations put in place under the Dodd Frank Act financial reforms; and (b) figure out ways to get around the Dodd Frank Act provisions – witness the BTO.

The profit motive is perfectly understandable. If I can invest in something that pays more than a Treasury bill or bond, or more than a corporate bond, then why not? However, at this point, as an investor, I need to make a decision – Am I investing or speculating? If I’m investing then it would make more sense to take a lower yield on something that has a more credible value. If I’m speculating (gambling) then why not borrow some money and purchase some exotic structured financial product the value of which is far less credible (or even comprehensible) and “make more money?”

It’s speculation that tends to get us into trouble. This new round of creative financial products shows all the elements that got us into financial trouble the last time in recent memory. Formulaic determination of value which ran head first into the wall of reality. Valuations which were based on “what’s good for business,” rather than on what might be other plausible outcomes. Emphasis on speculation rather than investment – or on financialism rather than capitalism. Short term yields as opposed to long term investment.

It was a recipe for trouble in 2007-2008 and it’s still a recipe for trouble in 2015.